How does whole life insurance work?

Life insurance can be a difficult topic. The subject is complicated, the options are many, and we often feel uncomfortable planning for the end of life. In addition, while most people recognize the value of life insurance, many are unsure about which type is best for them.

One common question people have is, “What is whole life insurance?” Whole life insurance is worth it for some people, but there are many plans to choose from. Read this guide to learn what choices are right for you, including whole life insurance costs, policies, and benefits.

Table of Contents

What Is Whole Life Insurance?

Whole life insurance is a permanent life insurance policy. It’s guaranteed to remain in force for the life of the insured as long as the premiums are paid. When you first apply for coverage, you are agreeing to a contract in which the insurance company promises to pay your beneficiary a certain amount of money – called a death benefit – when you pass. You’ll choose your coverage amount, and your premium will be calculated based on your age, gender, and health. As long as you pay your premiums, your whole life insurance policy will stay in effect and your premiums will remain the same regardless of health or age changes.

For example, let’s say you buy a whole life insurance policy at age 40. When you purchase the policy, the premiums will be locked in for the life of the policy as long as you pay them. They will be higher than the premiums of a term life insurance policy because your entire lifetime is built into the calculation.

Unlike term insurance, whole life policies don’t expire. The policy will stay in effect until you pass or until it is cancelled.

Over time, the premiums you pay into the policy start to generate cash value, which can be used under certain conditions. Cash value can be withdrawn in the form of a loan or it can be used to cover your insurance premiums. All loans must be repaid before you pass or they will be deducted from the policy’s death benefit.

How Does the Cash Value Benefit Work?

Whole life policies are one of the few life insurance plans that build cash value. What is whole life insurance cash value? It is generated when premiums are paid – the more premiums that have been paid, the more cash value there is. The main benefit of cash value is that it can be withdrawn in the form of a policy loan.

For example, if you have been paying premiums for many years and have an unexpected medical bill or financial obligation, you can call your insurance company and see how much you can withdraw from your policy. As long as the loan and any interest is repaid, your policy’s full coverage amount will be paid out to your beneficiary. If the loan isn’t repaid, the death benefit will be reduced by the outstanding balance of the loan.

What Is Whole Life Insurance as an Investment?

While whole life insurance policies act as an investment vehicle of sorts because of the cash value they accrue, you shouldn’t view any type of life insurance as an investment. True investments are heavily regulated and have safeguards in place to protect investors. While life insurance is also heavily regulated, its regulations have little to do with the financial sector.

Rather, you should view whole life insurance as a safeguard that protects your loved ones from experiencing a financial burden when you pass. The death benefit can help ensure they don’t have to dip into their savings or investments to handle your final arrangements.

What Does Whole Life Cover?

Whole life covers the entire life of the insured. When you have this policy type, it will provide a cash payout to your beneficiaries when you pass.

Costs & Premiums

Whole life insurance is more expensive than term life insurance because the insurer is insuring you for your entire life, not just for a term. And as you age, insuring you becomes more expensive.

Here is a chart that shows sample costs of a whole life insurance policy.

Whole Life Insurance Rates for a Male

| Age | $25,000 | $50,000 | $100,000 | $250,000 | $500,000 | $1MM |

|---|---|---|---|---|---|---|

| 50 | $65 | $116 | $217 | $531 | $1,057 | $2,101 |

| 55 | $80 | $144 | $276 | $678 | $1,351 | $2,688 |

| 60 | $102 | $182 | $350 | $865 | $1,725 | $3,436 |

| 65 | $130 | $234 | $454 | $1,123 | $2,241 | $4,468 |

| 70 | $174 | $314 | $611 | $1,518 | $3,031 | $6,047 |

| 75 | $237 | $429 | $840 | $2,090 | $4,176 | $8,337 |

Whole Life Insurance Rates for a Female

| Age | $25,000 | $50,000 | $100,000 | $250,000 | $500,000 | $1MM |

|---|---|---|---|---|---|---|

| 50 | $52 | $92 | $173 | $421 | $837 | $1,661 |

| 55 | $65 | $117 | $222 | $544 | $1,084 | $2,153 |

| 60 | $82 | $149 | $287 | $705 | $1,406 | $2,799 |

| 65 | $107 | $196 | $378 | $935 | $1,865 | $3,717 |

| 70 | $143 | $264 | $514 | $1,274 | $2,544 | $5,074 |

| 75 | $199 | $370 | $725 | $1,802 | $3,599 | $7,184 |

Whole Life vs. Term Life

As you begin to research your life insurance options, you’ll most likely come across the two main types of life insurance: term vs whole life insurance. Here are their basic definitions:

Term life insurance: This is insurance you buy to cover a specific term, such as 10 or 20 years. These policies do not accumulate cash value. Premiums tend to be lower because of the likelihood that you will outlive the policy. When the policy expires, you must buy another term and pay higher premiums if you still wish to have life insurance.

Whole life insurance: What is whole life insurance policies’ biggest benefit over term? This is insurance you buy for the length of your life. Unlike term insurance, whole life policies don’t expire. The policy will stay in effect until you pass or until it is canceled. The initial cost of premiums is higher than it is with term insurance because of the length of the policy. However, part of the premiums you pay builds up into cash value, which you can use later in life. With whole life insurance, the policy you buy at age 40 remains with you. Whole life insurance is often referred to as “permanent” insurance.

Here’s a chart showing the key differences between the two types of policy.

| Whole Life Insurance | Term Life Insurance |

|---|---|

| Provides a death benefit | Provides a death benefit |

| Only pays a death benefit if premiums are current | Only pays a death benefit if premiums are current |

| Coverage is for a lifetime as long as premiums are paid | Coverage is only for a term such as 5, 10, or 20 years |

| Premiums stay the same | Premiums go up every time you have to renew your policy |

| Has a cash value | Does not have a cash value |

| You can withdraw cash value as a loan | No option to borrow against the policy |

| More expensive premiums | Lower premiums when you’re young but they increase as you age |

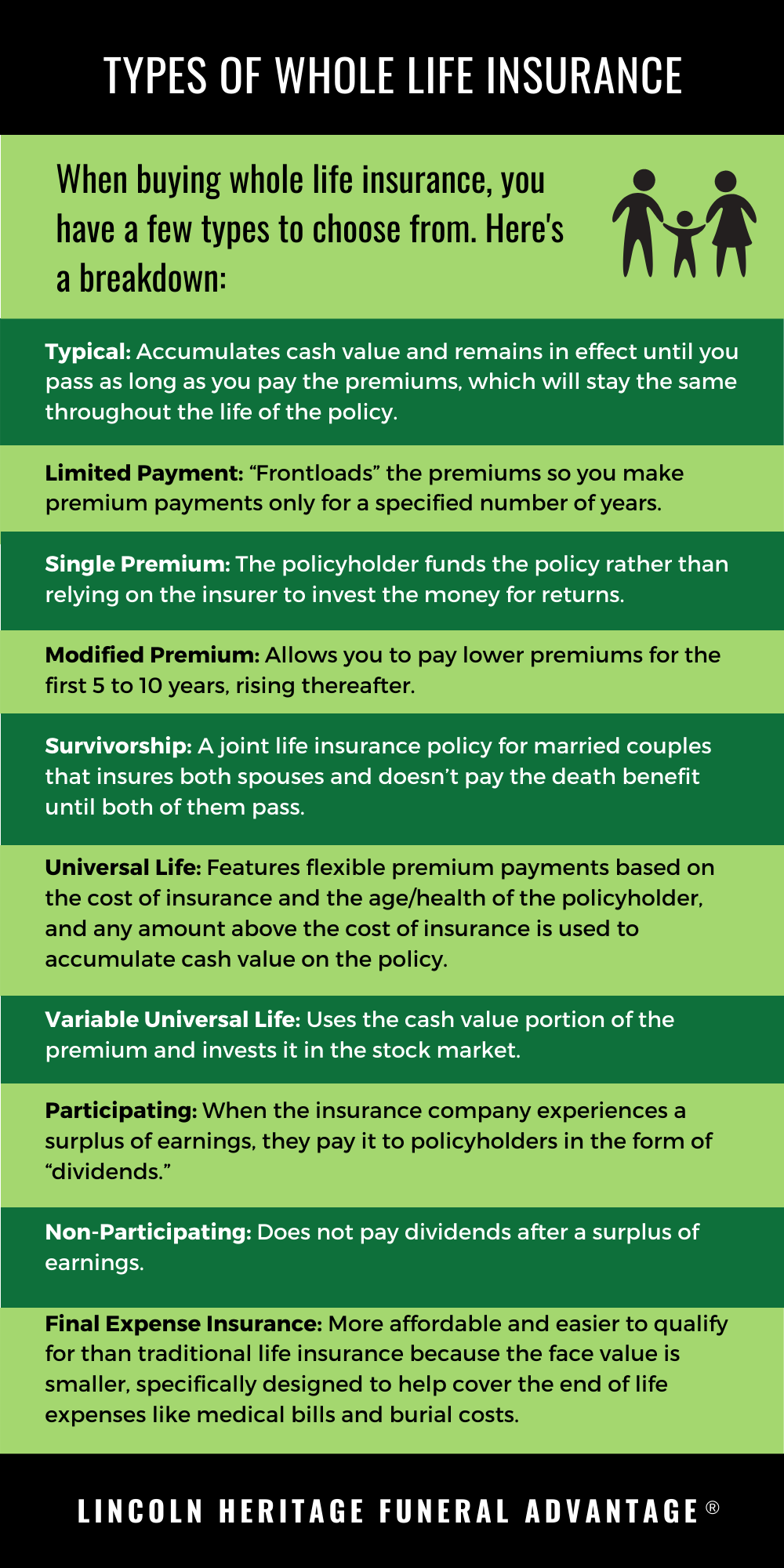

Types of Whole Life Insurance

When buying whole life insurance, you have a few types to choose from. Here is a breakdown of the various types of whole life insurance and the features and benefits of each.

Typical

This policy provides level premiums, so your rate stays the same for the life of the policy. It’s in effect until you pass as long as you pay the premiums. It also accumulates cash value, which increases the longer you own the policy.

Limited Payment

With this type of policy, you will make premium payments for a specified number of years – 10, 15, or 20 – and pay for the policy upfront. Doing this eliminates the need to pay premiums for the rest of your life. Instead, you frontload the premiums and enjoy a premium-free policy in the years after that.

Single Premium

To purchase a single-premium policy, you will need to pay a sum of money in exchange for a death benefit. For instance, you could pay $25,000 for a $50,000 death benefit. The more you pay, the higher the death benefit will be.

Modified Premium

Modified premium life insurance policies allow you to pay lower premiums for the first 5 to 10 years. After that, the premiums will rise. This type of policy is ideal for someone who wants to buy a policy with a high death benefit and knows they will be in a better position to pay higher premiums in the future.

Survivorship

Some married couples choose a joint life insurance policy called a survivorship policy. This type of policy insures both spouses and doesn’t pay the death benefit until both of them pass. For parents who worry that their special needs child won’t be cared for after they pass, a survivorship policy will ensure that the child has the funds needed. Also, some people use survivorship policies to ensure their adult children have enough money to pay estate taxes once both parents are gone.

Universal Life

A universal life insurance policy is a type of whole life insurance that features flexible premium payments. The payments are based on the cost of insurance, which includes administrative fees, mortality charges, and other charges that keep the policy in place. The cost of insurance depends on the age and health of the policyholder. As you age, the cost of your premiums will go up. Any amount you pay above the cost of insurance is used to accumulate cash value on the policy. If the cash value grows enough, it may cover the increase in premiums as you age.

Variable Universal Life

A variable universal life insurance plan works as a universal life policy with one difference. Instead of a guaranteed cash value, this type of policy uses the cash value portion of the premium and invests it in the market. That means the cash value can increase when the investments turn out well – or decrease when they don’t.

Participating or Non-Participating

Whole life insurance policies are either participating or non-participating. If your policy is participating, that means when the insurance company experiences a surplus of earnings, they pay it to policyholders in the form of “dividends.” The IRS does not tax these dividends because it views them as an overpayment on the insurance policy. If a whole life policy doesn’t pay dividends, it is considered a non-participating policy.

Final Expense Insurance

One of the most popular kinds of whole life insurance is called final expense insurance. Commonly known as burial insurance or funeral insurance, final expense plans are specifically designed to help cover end-of-life expenses like medical bills and burial costs.

Final expense policies typically have smaller face amounts – usually under $20,000 – because they are meant to cover specific expenses for surviving loved ones. Final expense plans can be more affordable and easier to qualify for than traditional life insurance because the face amount is so small.

Funeral Advantage is a final expense insurance program specifically designed to help cover final expenses – such as medical bills and funeral costs. Like everything today, the average funeral cost has been steadily rising. The average funeral can cost up to $9,000 depending on the services you use. Casket prices alone can be thousands of dollars depending on the material used.

Most families aren’t financially prepared to cover the high cost of their loved one’s final arrangements. That’s what Funeral Advantage is for. It provides a life insurance cash benefit when your family needs it most. Most of our policies range from $10,000 – $15,000, making them perfect for families on a fixed income who are concerned about paying for their loved one’s final arrangements. With Funeral Advantage, you don’t need to take a medical exam to qualify like most insurance policies. All you have to do is answer a few health questions on a one-page application.

Included with every Funeral Advantage policy is a free membership to the Funeral Consumer Guardian Society® (FCGS). The FCGS will help your surviving loved ones with the many details that will immediately arise upon your passing. They’ll help price shop funeral costs to protect your family from overspending.

Whole Life Riders

Many people are curious as to what is whole life insurance rider coverage. Whole life insurance riders are features you can add to certain whole life policies that boost its features and benefits. There are four riders that you can consider when buying whole life insurance.

- Waiver of premium: A waiver of premium rider ensures that the policy premium is paid if the policyholder becomes disabled.

- Accelerated death benefit: If a policyholder becomes terminally ill and has less than a year to live, the insurance company will pay them a portion of the face value of their insurance policy before they pass. For instance, if you have a $1 million policy, the insurance company may pay you $750,000. Some insurers automatically include this rider in all of their policies for no additional fee, so be sure to check yours.

- Term life rider: If you have a whole life insurance policy and want to increase the death benefit, one way to do it is to add a term life rider. This rider allows you to add a term life insurance policy to your whole life policy and increase the amount of the death benefit for less than you would have to pay if you increased it on the whole life policy.

- Guaranteed purchase option rider: This rider allows you to buy additional life insurance without having to take a medical exam. For instance, if a healthy 30-year-old has this rider, he can add $50,000 more in insurance when he reaches age 60 without a medical exam.

Myths & Misconceptions

Most people think about buying life insurance at some point in their life, and may have heard some myths and misconceptions that prevent them from doing it.

Here are misconceptions about whole life insurance that we encounter often:

- You have to be in perfect health to get life insurance. The truth is you can purchase life insurance no matter what kind of health you are in. There are plenty of no medical exam policies and guaranteed acceptance plans on the market. There are also policies that only ask health questions on the application.

- Life insurance is too expensive for seniors. While it’s true that a whole life policy with a large death benefit will cost a lot in monthly premiums, you can purchase final expense insurance for a fraction of the cost. If you want a policy that will cover your burial costs and other final expenses, this is an ideal solution. People who purchase life insurance for parents who are aging or in poor health often choose these policies to help with the costs once they pass. Be sure to research multiple providers so you can find the best life insurance for seniors.

- Term insurance is better than whole life insurance. Many people assume term insurance is better because it’s often cheaper. But price is just one factor to consider. Term insurance plans may take longer to pay out depending on the size of the policy. And if you take out a term policy in your 30s, but need to renew in your 60s, your rate will be extremely high.

FAQs

Is whole life insurance worth it?

Whole life insurance is worth buying for many people. While it’s typically more expensive than term life insurance, as long as your premiums are paid, it offers permanent coverage with premiums that never change regardless of your health or age. It also builds cash value over time, giving you the opportunity to take out a loan from your policy to pay for medical bills or other expenses.

What happens when a whole life insurance policy matures?

Most whole life policies endow at age 100. When a policyholder outlives the policy, the insurance company may pay the full cash value to the policyholder (which in this case equals the coverage amount) and close the policy. Others grant an extension to the policyholder who continues paying premiums until they pass. Others still stop collecting premiums, but keep the policy active until it’s needed.

Can you cash out a whole life policy?

Yes. You can surrender the policy and exchange it for the value. You can take a loan against the cash value, which may or may not incur interest, depending on the insurer.

How do I withdraw money from my whole life policy?

If you choose to withdraw money from your whole life insurance policy, simply contact your insurer to see how much is available, what interest rate will be applied (if any), and whether you will be taxed on the loan.

What is whole life insurance for seniors?

While seniors may qualify for a variety of policy types depending on their age and health, final expense policies are often referred to as senior policies. That’s because they’re available to those who are too old or in too poor health to buy other insurance. Even those in their 70s can find coverage, with many policies only requiring a brief health questionnaire rather than a physical exam.

What happens to whole life insurance at age 100?

Many whole life insurance policies are written to expire at age 100. But if you live longer than that, you have a couple of options. For instance, if you are younger than 85, you could do a 1035 exchange into a new policy that lasts until age 121. And if you’re in your 90s, you may be able to do a 1035 exchange into a deferred annuity with the cash value of your policy. But before you do anything, you should talk to your financial planner and insurance agent to help you make the best decision.

Next Steps

Every individual or family has different concerns and questions about which kind of life insurance is most suited for them, how much coverage they need, and which policy will best provide for their needs and the needs of their loved ones. Whole life insurance costs more than term life insurance in many cases, but because of its smaller policy size, final expense insurance is an affordable option for individuals needing coverage for end-of-life expenses. If you’re wondering what is whole life insurance vs. term life insurance benefits for your unique situation, working with an insurance agent will help you decide if whole life insurance is worth it when it comes to your needs and wishes.

At Lincoln Heritage Life Insurance Company®, we specialize in meeting with you one-on-one to learn what your needs are. We’ll take the time to understand your situation and help you protect your loved ones.